Global Coal Output at Record High – Coal Prices High – China Leads the Way – The International Energy Agency is established; a United Nations Treaty under Belgian Law - [12-31-24]

Direct from BOOM Finance and Economics

Hat Tip to my colleague at BOOM Fin4ance and Economics Substack (Subscribe for Free) - also on LinkedIn and WordPress. Covid Medical News Network CMN News BOOM Blog and All Editorials (over 5 years) at BOOM Finance and Economics | Designed for Critical Thinkers — UPDATED WEEKLY (WordPress.com)

BOOM Finance and Economics seeks out the very best information from authoritative sources and strives for consistency in its quality and trustworthiness. Over 5 years, BOOM has developed a loyal readership which includes many of the world’s most senior economists, central bankers, their senior advisers, fund managers, and academics. If you want a real edge in understanding the complex world of finance and economics, subscribe to BOOM on Substack or as a Follower on LinkedIn.

BOOM EDITORIAL THIS WEEK

GLOBAL COAL CONSUMPTION AT RECORD HIGH. The International Energy Agency (AEI) released its latest report on Coal last week. It is imaginatively titled Coal – 2024. The report is 127 pages long. BOOM has read it so you don’t have to, and presents the most pertinent facts.

THE KEY OBSERVATION: Despite much propaganda to the contrary, COAL IS NOT IN DECLINE and is essential for the global energy mix. In 2024, global consumption was at record highs. Prices are also at high levels historically.

BUT what happened to Global Warming? Who knows? Recent data from the National Oceanic and Atmospheric Administration (NOAA) has revealed that the Arctic sea ice extent is 26% greater than it was in 2012; thus contradicting dire climate predictions from previous years, according to climate sceptic Tony Hellyer.

In 2007, a BBC News article (worth reading) titled “Arctic summers ice-free ‘by 2013”, claimed that northern polar waters could become ice-free within six years based on computer modelling studies. Mmmmm... BBC Quote 2007: “Using supercomputers to crunch through possible future outcomes has become a standard part of climate science in recent years.” Gee whiz, super computers!

Professor Peter Wadhams, best known for his work on sea ice, was quoted in the 2007 article as saying “In the end, it will just melt away quite suddenly”. He is emeritus professor of Ocean Physics, and Head of the Polar Ocean Physics Group in the Department of Applied Mathematics, and Theoretical Physics, University of Cambridge. BOOM says… Mmmmm

However, the latest NOAA Technical Report dated December 2024 states “Sea ice extent in September 2024 was the 6th lowest in the satellite record (1979 to present); the last 18 September extents (2007-24) are the 18 lowest in the record.” And “Snow accumulation during the 2023/24 winter was above the 1991-2020 average across both the Eurasian and North American Arctic. Early snow onset and delayed spring melt resulted in a longer than average snow season over much of the Eurasian Arctic.”

THE COAL REPORT 2024. The IEA Coal report analyses the latest trends in coal production and demand and updates medium-term forecasts. It shows that global coal use has rebounded strongly after plummeting at the height of the Covid Panic-Demic. Total coal consumption is expected to reach 8.77 billion tonnes in 2024. This is a record high. Global consumption of coal has doubled in the past three decades which would be a surprise to most ill-informed Western politicians and the mainstream media who are all convinced in the opposite view.

The electricity sector in China is particularly important to global coal markets, with one third of coal consumed worldwide burned at a power plant in China. China consumes 30% more coal than the rest of the world put together. Demand for coal is increasing in emerging economies where electricity demand is rising sharply along with economic and population growth, as in India, Indonesia and Viet Nam. In emerging economies, growth is mainly driven by coal demand from the power sector, although industrial use is also increasing.

In absolute terms, the most significant increases in demand in 2024 have been in India (up 6%) and China (up 1.1%), together with others like Indonesia and Viet Nam.

Conversely, the largest declines have taken place in the European Union (down 12%) and the United States (down 5%).

HIGH COAL PRICES. Coal prices today are 50% higher than the average seen between 2017 and 2019.

Coal production reached an all-time high in 2024. Asia remains the centre of the international coal trade, with all of the largest importing countries in the region, including China, India, Japan, Korea, and Viet Nam, while the largest exporters include Indonesia and Australia.

Amid the energy crisis of 2022, thermal coal prices surged to unprecedented levels, driven by tight supply-demand fundamentals, soaring natural gas prices and geopolitical risks. High-CV thermal coal benchmarks exceeded the US$400/t mark multiple times, far surpassing previous records. Notably, for over six months’ thermal coal prices outstripped those of coking coal, an unusual development.

However, as coal markets began to stabilise in 2023, following trends in other energy commodities, coking coal prices once again surpassed thermal coal, with the average annual premium returning to historical norms. The appreciation of the US dollar has had an impact on coal trade. International coal trade is mainly priced in US dollars, making exchange rates a crucial factor in the competitiveness of coal traded.

When a currency depreciates against the US dollar, it generally increases the cost of coal for buyers, making purchases more expensive. This fuels Global CPI inflation in energy importing nations. In effect, America exports inflation through US dollar dominance and strength.

US DOLLAR RISING AND RISING – US dollar Index over 5 years

Can you see the US Dollar Collapse so often referred to by countless financial “gurus” and economic “experts” on the Net? No, neither can BOOM. US dollar strength is the problem.

CHINA LEADS THE WAY – MADE IN CHINA FROM COAL. Coal demand in China remains strong. China, the world’s largest coal consumer, used 4,883 MT of coal in 2023, marking a 6% y-o-y increase and accounting for 56% of global coal consumption. The majority (85%) of this consumption was thermal coal, amounting to 4,146 MT, primarily used for power generation. The remaining 737 MT was metallurgical coal (met coal).

China produces solar panels, windmill components and electric cars for markets in Western Europe, the UK, the USA and other “advanced” economies. All of those products are principally made using coal as the energy source. In China, more than half of the primary energy comes from coal. Perhaps we should use the term “Made in China from Coal” to describe the “Renewables” energy sector and electric car sales in the advanced economies?

In the global car market, China made over 30 million cars in 2023, 32.2% of total global production - Germany made 4 Million.

In China, 74% of thermal coal demand is used in power plants to create electricity. The Chinese electricity sector is the main driver of China’s coal demand and consequently global coal demand.

CHINA’S NEW COAL FIRED POWER PLANTS — 220 OF THEM. During 2022-23 China approved around 220 GW of new coal-fired power/electricity capacity. Acting on this, it began construction of 70 GW in 2023 and an additional 41 GW in the first half of 2024. Worldwide there are around 2,500 coal-fired power stations, on average capable of generating a Gigawatt each, and they generate about a third of the world’s electricity.

So — as the Americans say “do the Math” — China is planning to build an extra 220 Coal-Fired Power stations while the West is shutting theirs down in the pursuit of Climate Virtue Signalling amid economic destruction.

China also converts coal into other commodities, typically through coal gasification and liquefaction. In this way, coal imported by China produces Fertiliser to boost food production, Synthetic Natural Gas, Polyester, Olefins, Diesel Fuel and Gasoline.

COAL CONSUMPTION IN AMERICA IS FALLING. In the United States overall coal consumption is expected to have decreased from 386MT in 2023 to 368MT in 2024, a decline of 5%, slower than the 17% fall seen in 2023.

COAL CONSUMPTION IN EUROPE AND UK IS FALLING. Coal consumption is declining in Europe. In 2023, the Republic of Türkiye surpassed Germany and Poland to become the largest consumer of coal in Europe. Its total coal consumption in 2024 is expected to rise by 2.8% from the 2023 level to 129MT. Turkey will soon commission its first Nuclear Power Plant, Akkuyu. It is expected to generate around 10% of the country’s electricity when completed. The plant is being built by Rosatom, a Russian company.

In May 2010, Russia and Türkiye signed an agreement that a subsidiary of Rosatom would build, own, and operate the Akkuyu power plant comprising four 1,200 MWe VVER1200 units. It is expected to be the first ‘build–own–operate’ nuclear power plant in the world.

UK CLOSES ITS LAST COAL FIRED POWER PLANT. Meanwhile, in September 2024, the United Kingdom’s last coal-fired power plant, Ratcliffe-on-Soar, ceased operations, marking the end of 142 years of coal fired power production. The world’s first coal-fired utility power plant began generating electricity in the UK in 1882.

COAL CONSUMPTION IN SOUTH EAST ASIA IS UP 8%. Strong demand for coal in Southeast Asia is being driven by Indonesia and Viet Nam. Coal consumption in ASEAN countries reached 457MT in 2023, marking a 10% increase from the previous year. Of this, 76% was used for electricity generation. Indonesia accounted for nearly half (48%) of ASEAN countries’ coal use, followed by Viet Nam (21%), the Philippines (9%) and Malaysia (8%).

For 2024, ASEAN coal consumption is expected to rise to 491MT (up 8%). As in previous years, increased demand in Indonesia is the main reason for this uplift. The region continues to have robust economic growth prospects, accompanied by numerous coal-fired power plants currently under construction. Demand for coal in ASEAN countries is expected to grow by 5% annually and reach 567MT by 2027. Indonesia accounts for two-thirds of this growth.

Coal Consumption Fuelled by electric cars and batteries. Growing coal consumption in Indonesia is mainly fuelled by power generation, but also by nickel production. In 2023 Indonesia produced 1.9MT of nickel, over half of global output. With rising demand for electric vehicles, and batteries for other uses, investment in Indonesia’s nickel production capacity is increasing.

Indonesia is also expanding aluminium production in order to export aluminium rather than bauxite. A new industrial park in North Kalimantan is due to result in the country’s aluminium production growing to 2.5MT pa, increasing electricity demand by around 30 TWh. The country has the world’s fourth-largest population and is set to become the fourth-largest coal consumer too.

COAL CONSUMPTION IN AFRICA RISING. South Africa’s coal sector is at a crossroads. In 2024, coal consumption in Africa is expected to increase by 6mt to a total of 191mt, driven mainly by the improved performance of coal-fired assets operated by Eskom, the state-owned power utility. The country accounted for 86% of Africa’s coal consumption in 2023 and is expected to have increased its coal consumption to 165mt in 2024. Economic activity in South Africa has seen a slight improvement, and a reduction in load shedding is expected to increase coal demand.

Despite a projected increase of over 50% in nuclear generation and a doubling of renewable generation, strong electricity demand growth is expected to create room for an additional 14TWh of coal-fired generation in South Africa in the next three years. The country continues to run three coal-fired power plants of 4.5GW capacity that were previously set for closure.

The lifetime of the three plants will be extended until 2030. Consequently, South Africa’s coal consumption for power generation is expected to rise to 124Mt by 2027.

In March 2024, a steel plant operated by China’s Tsingshan Group began commercial operations in Zimbabwe. The initial output is 0.6Mt of steel per year. The long-term goal is to reach a production capacity of 5Mt, positioning Zimbabwe as the continent’s leading steel producer. This will increase annual coking coal demand by 0.4Mt with a further potential of up to 4Mt. In Zambia two new coal-fired units have received approval after the power cuts following the droughts suffered in the country during 2024.

COAL CONSUMPTION IN INDIA – 10% GROWTH P.A. After surpassing the one billion tonne mark in 2023, India’s coal production growth is set to continue. In 2023, Indian coal production increased by 10%.

COAL PRODUCTION IN AUSTRALIA EXPANDING. Australian coal production is largely export oriented, as only a fifth of its coal output is consumed domestically. The domestic market has been declining for over a decade so export expectations have driven investment.

In 2023, Australian coal production increased by 6% to 459Mt. New mines came into operation during 2024, including the Dartbrook mine, the Olive Downs Complex and the open pit Vickery mine.

Metallurgical coal exports, of which Australia is the largest exporter by far, are expected to shrink. In addition, Mongolia stepped up to become the second-largest exporter of met coal in 2024, reducing China’s appetite for Australian exports.

Australia continues to dominate the project list for new or expanding coal mining projects aimed at exports. Australia has a total of 47 projects at both the less advanced and more-advanced stages, with most targeting the production of metallurgical coal or a mix of with thermal coal. Australia’s share of new or expanding projects in the global pipeline stands at 62%.

COAL PRODUCTION IN THE UNITED STATES IS FALLING. Coal production in America fell by 2.8% in 2023, although the decline in domestic demand was much stronger. In 2024, coal production is expected to fall by 12%.

COAL PRODUCTION IN EUROPE IS PLUMMETING. EU coal production plummeted in 2023 and the decline is expected to continue through to 2027. In the European Union more than 80% of overall coal production is lignite. Lignite is mostly consumed in power plants close to the mines. Therefore, in 2023 lignite production has declined in line with lignite-fired power generation.

Germany, the country with the largest power sector and highest potential for fuel-switching, saw the strongest decline across EU countries (down 29Mt). In relative terms, coal production decreased the most in Bulgaria, by 41% or 15Mt. In Poland both lignite and steam coal declined (down 16Mt combined), due to lower demand and the high cost of steam coal compared with the price of imported coal. Czechia was observed to decline as well (down 5Mt). The result was total coal output of 278Mt in the European Union in 2023.

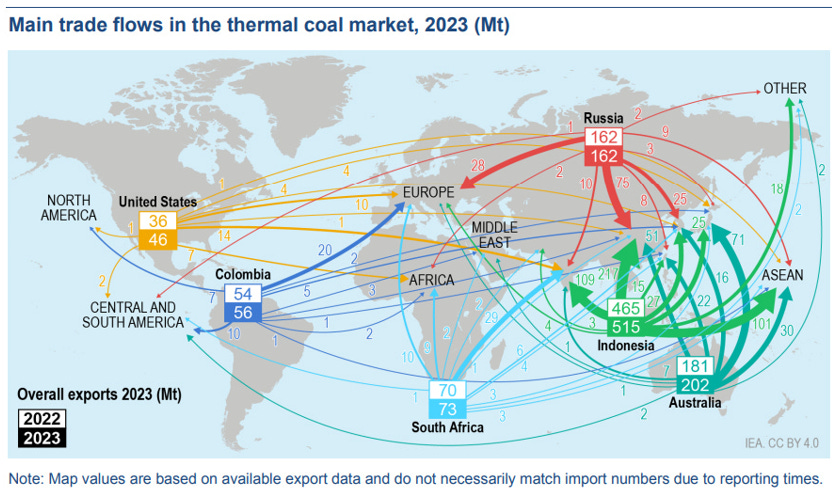

INTERNATIONAL COAL TRADE — DOMINATED BY ASIA. International coal trade is set for another all-time high in 2024 having risen by 10% in 2023, reaching a total of 1,510Mt. Growth was recorded in the trade of both thermal coal (up 100Mt) and met coal (up 42Mt). Trade accounted for about 17% of global coal demand and more than three-quarters of traded coal was thermal coal. Seaborne trade accounted for more than 90% of all traded coal in 2023, although land-based trade saw an increase during the year. The Asia Pacific region once again increased its share of global coal imports, accounting for 84% of the total coal trade during 2023.

China saw the highest imports of coal in 2023 at around 481Mt, followed by India (248Mt) and Japan (167Mt). Combined, these three countries received almost 60% of global coal imports in 2023. The largest exporters were Indonesia (521Mt), serving mostly thermal coal, Australia (353Mt) and Russia (211Mt), with a combined share of almost three-quarters of global coal exports in 2023.

Both Chinese imports and Indonesian exports reached levels never achieved by any country before. Notably, Russian exports saw a significant shift to the east during 2023, following the EU ban on Russian coal imports in 2022. While two-thirds of Russian exports were directed to Asian markets in 2022, this share surged to about 84% during 2023. In 2024, global trade in coal is expected to reach a new all-time high of 1,545Mt.

COAL TRADE FLOWS – METALLURGICAL COAL (Met Coal)

TOTAL COAL IMPORTS. This chart summarises the global situation. In the last year, the Asia-Pacific Region increased its coal imports by 5.6%. China increased its imports by 9.6%.

Europe’s coal imports declined by 18.3% — a staggering collapse. This is indicative of a European economy in recession.

The International Energy Agency (IEA) Disclaimer — This work reflects the views of the IEA Secretariat but does not necessarily reflect those of the IEA’s individual member countries or of any particular funder or collaborator. The work does not constitute professional advice on any specific issue or situation. The IEA makes no representation or warranty, express or implied, in respect of the work’s contents (including its completeness or accuracy) and shall not be responsible for any use of, or reliance on, the work.

Source: https://www.iea.org/reports/coal-2024

THE IEA IS A UNITED NATIONS TREATY UNDER BELGIAN LAW. In late 1974, a United Nations Treaty called the Agreement on an International Energy Program (IEP) was signed by a number of Nation States. The Treaty established the International Energy Agency (IEA) and was clearly global in its stated goals. Its Executive Director is Fatih Birol, born in Ankara, Turkey in 1958. Readers should note that he is also chairman of the World Economic Forum’s (Davos) Energy Advisory Board.

The World Economic Forum (WEF) is a private, unelected, non-governmental organisation established by Klaus Schwab and meets annually in Davos, Switzerland by private invitation only. BOOM wonders why the IEA allows its Executive Director to be an adviser to a private Think Tank?

Before joining the IEA, Dr Birol worked at the Organization of the Petroleum Exporting Countries (OPEC) in Vienna. He completed a BSc degree in power engineering from the Technical University of Istanbul and also has an MSc and PhD in energy economics from the Technical University of Vienna.

The Agreement on an International Energy Program was “registered by Belgium on May 12, 1977”. Presumably, this is therefore a contractual agreement under Belgian Law.

“Each Signatory State shall, not later than May 1, 1975, notify the Government of the Kingdom of Belgium that, having complied with its constitutional procedures, it consents to be bound by this Agreement.”

The original document contains the following introduction: “The Governments of the Republic of Austria, the Kingdom of Belgium, Canada, the Kingdom of Denmark, the Federal Republic of Germany, Ireland, the Italian Republic, Japan, the Grand Duchy of Luxembourg, the Kingdom of the Netherlands, Spain, the Kingdom of Sweden, the Swiss Confederation, the Republic of Turkey, the United Kingdom of Great Britain and Northern Ireland, and the United States of America,

Desiring to promote secure oil supplies on reasonable and equitable terms. Determined to take common effective measures to meet oil supply emergencies by developing an emergency self-sufficiency in oil supplies, restraining demand and allocating available oil among their countries on an equitable basis, Desiring to promote co-operative relations with oil producing countries and with other oil consuming countries, including those of the developing world, through a purposeful dialogue, as well as through other forms of co-operation, to further the opportunities for a better understanding between consumer and producer countries, Mindful of the interests of other oil consuming countries, including those of the developing world, Desiring to play a more active role in relation to the oil industry by establishing a comprehensive international information system and a permanent framework for consultation with oil companies, Determined to reduce their dependence on imported oil by undertaking long term co-operative efforts on conservation of energy, on accelerated development of alternative sources of energy, on research and development in the energy field and on uranium enrichment, Convinced that these objectives can only be reached through continued cooperative efforts within effective organs, Expressing the intention that such organs be created within the framework of the Organisation for Economic Co-operation and Development, Recognising that other Member countries of the Organisation for Economic Cooperation and Development may desire to join in their efforts, Considering the special responsibility of governments for energy supply, Conclude that it is necessary to establish an International Energy Program to be implemented through an International Energy Agency, and to that end, Have agreed as follows:

Article 1. 1. The Participating Countries shall implement the International Energy Program as provided for in this Agreement through the International Energy Agency, described in Chapter IX, hereinafter referred to as the “Agency”.

2. The term “Participating Countries” means States to which this Agreement applies provisionally and States for which the Agreement has entered into and remains in force. 3. The term “group” means the Participating Countries as a group.”

Key requirements under the IEP treaty are that member countries:

· hold oil stocks equivalent to at least 90 days of their prior year’s daily net oil imports and

· in the event of a major oil disruption, contribute to IEA collective actions by way of a stock release, demand restraint, fuel switching, increased production or fuel sharing.

Nations can leave the IEA if they Notify the King of Belgium under Article 69.2 Any Participating Country may terminate the application of this Agreement for its part upon twelve months’ written notice to the Government of the Kingdom of Belgium.

GENEROUS ANNUAL BUDGET

To achieve these goals, the IEA has a Budget of over $60 million p.a. This is a very generous sum indeed.

ORIGINAL SIGNATORIES AND MEMBERS. The original signatories to the agreement were Austria, Belgium, Canada, Denmark, Germany, Ireland, Italy, Japan, Luxembourg, the Netherlands, Spain, Sweden, Switzerland, Turkey, United Kingdom, United States of America. Nations that have joined later include Australia, Portugal and Greece.

The only Member nations that export energy are Canada and the United States. The vast majority of energy exporting nations do NOT belong to the IEA.

Member Countries

· Australia Austria Belgium Canada Czechia Denmark Estonia Finland France Germany Greece Hungary Ireland Italy Japan Korea Latvia Lithuania Luxembourg Mexico New Zealand Norway Poland Portugal Slovak Republic Spain Sweden Switzerland The Netherlands Türkiye United Kingdom United States

Accession countries

· Colombia, Costa Rica, and Chile.

Association countries

· Argentina, Brazil, China, Egypt, India, Indonesia, Kenya, Morocco, Senegal, Singapore, South Africa, Thailand, and Ukraine.

Source: https://treaties.un.org/doc/Publication/UNTS/Volume%201040/volume-1040-I-15664-English.pdf

COMING NEXT:

· The Financial Jigsaw Part 2 – THE HEARTLAND THEORY - Saturday, January 4, 2025

· BOOM Global Financial Review, Tuesday January 7, 2025

In economics, things work until they don’t. Make your conclusions and do research. BOOM does not offer investment advice.

CLICK HERE FOR PODCASTS: OUR BRAVE NEW ECONOMIC WORLD

BANKS DON’T TAKE DEPOSITS, THEY BORROW YOUR MONEY: LOANS CREATE DEPOSITS — this is how almost all new money is created in the economy (by commercial banks making loans). https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy. Watch the short 15-minute video and see Professor Richard Werner brilliantly explaining how global banking systems work.

In 2014, Richard Werner provided the first empirical evidence that banks create credit out of thin air. They do this whenever they issue a loan or, more specifically, purchase a promissory note. This is a walk-through of exactly how they do it.

Many economists are unaware of this and even ignore the banking & finance sectors in their econometric models. Prof Richard Werner explains how things are going now with CBDCs:

DISCLAIMER: All content is presented for educational and/or entertainment purposes only. Under no circumstances should it be mistaken for professional investment advice, nor is it at all intended to be taken as such. The commentary and other contents simply reflect the opinion of the authors alone on the current and future status of the markets and various economies. It is subject to error and change without notice. The presence of a link to a website does not indicate approval or endorsement of that website or any services, products, or opinions that may be offered by them.

Neither the information nor any opinion expressed constitutes a solicitation to buy or sell any neither securities or investments. Do NOT ever purchase any security or investment without doing your own and sufficient research. Neither BOOM Finance and Economics.com nor any of its principals or contributors are under any obligation to update or keep current the information contained herein. The principals and related parties may at times have positions in the securities or investments referred to and may make purchases or sales of these securities and investments while this site is live. The analysis contained is based on both technical and fundamental research.

Although the information contained is derived from sources that are believed to be reliable, they cannot be guaranteed.

Disclosure: We accept no advertising or compensation, and have no material connection to any products, brands, topics or companies mentioned anywhere on the site.

Fair Use Notice: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of issues of economic and social significance. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. By Title 17 U.S.C. Section 107, the material on this site is distributed without profit. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

So our leaders in the UK (and others) are determined to destroy that which our parents and Grandparents fought to build and maintain. It cannot be too long before there is a revolt, when Net Zero stupidity begins to bite.

"Can you see the US Dollar Collapse so often referred to by countless financial “gurus” and economic “experts” on the Net?" (Boom)

Whilst I claim no financial expertise, a US National Debt of $36 trillion suggests to me a collapse at some time, is inevitable, unless the US Taxpayers can work out how to pay $272,000 each (figures from US debt clock).

As for coal, dig baby dig - we've got lots of it.

Chana is clever using up cheap coal while funding the enviornMENTALists in the West.